USDT vs Bank Transfer: Which Is Better for International Payments in 2026?

Keywords: USDT Payments, Stablecoin Payments, USDT vs Bank Transfer, Cross Border Payments, International Money Transfer, Global Payments, Send Money Internationally

Introduction

Sending money internationally has never been more important.

Freelancers receive payments from overseas clients. Businesses pay international suppliers. Remote workers earn salaries from companies located in different countries.

For decades, international bank transfers have been the standard method for moving money globally.

However, the rise of stablecoins such as USDT is changing how people think about cross-border payments.

Today, many businesses and individuals are asking:

Should I use a traditional bank transfer or USDT?

In this guide, we'll compare USDT and bank transfers across speed, cost, accessibility, transparency, and practical use cases to help you determine which solution is best for international payments in 2026.

What Is a Bank Transfer?

A bank transfer is the movement of money between financial institutions.

For international payments, transfers typically move through:

- SWIFT Network

- Correspondent Banks

- Receiving Banks

This system has been the backbone of global finance for decades.

Common use cases include:

- Business payments

- Supplier settlements

- International payroll

- Personal remittances

What Is USDT?

USDT (Tether) is the world's largest stablecoin.

Unlike cryptocurrencies that fluctuate significantly in value, USDT is designed to maintain a value close to 1 US Dollar (USD).

This makes USDT attractive for:

- International transfers

- Cross-border payments

- Digital commerce

- Global settlements

USDT can be transferred through multiple blockchain networks, including:

- TRC20 (TRON)

- ERC20 (Ethereum)

- BEP20 (BNB Chain)

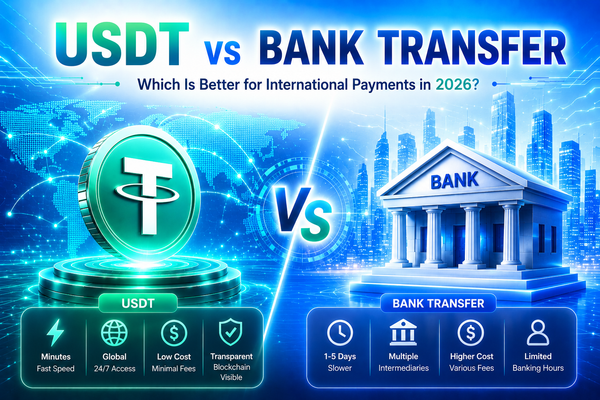

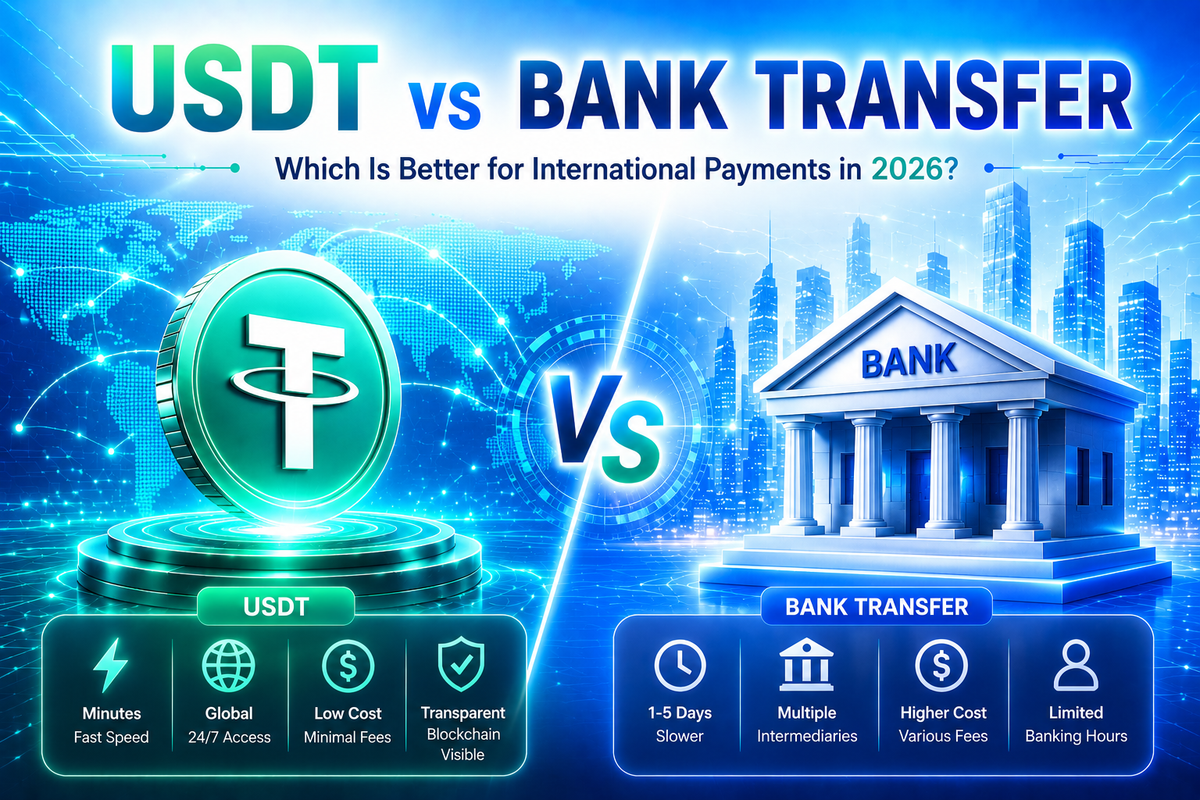

USDT vs Bank Transfer: Quick Comparison

| Feature | Bank Transfer | USDT |

|---|---|---|

| Settlement Speed | 1–5 Business Days | Minutes |

| International Access | Depends on Banks | Global |

| Operating Hours | Banking Hours | 24/7 |

| Intermediaries | Multiple | Minimal |

| Transparency | Limited | Blockchain Visible |

| Transfer Fees | Varies | Network Fees |

| Weekend Transfers | Limited | Yes |

| Cross-Border Payments | Yes | Yes |

Speed Comparison

Bank Transfer

International transfers often require:

Sending Bank

↓

Correspondent Bank

↓

Receiving Bank

Each institution adds processing time.

Typical Processing Times

- Domestic Transfers: Same Day to 1 Business Day

- International Transfers: 1–5 Business Days

Payments may take longer due to:

- Compliance reviews

- Banking holidays

- Time zone differences

USDT

USDT transactions occur on blockchain networks.

TRC20

Typical confirmation time:

1–3 minutes

BEP20

Typical confirmation time:

1–5 minutes

ERC20

Confirmation times depend on network congestion.

In most situations, funds arrive significantly faster than traditional international transfers.

Cost Comparison

Bank Transfer Costs

International bank transfers may involve:

Sending Fees

Charged by the originating bank.

Receiving Fees

Charged by the receiving bank.

Intermediary Fees

Deducted by correspondent banks.

FX Conversion Fees

Applied when currencies are exchanged.

These costs can accumulate quickly for businesses and individuals making frequent international payments.

USDT Costs

USDT transfers generally involve blockchain network fees.

Examples include:

TRC20

Often among the lowest-cost options.

BEP20

Typically low-cost.

ERC20

Can become expensive during periods of network congestion.

Because there are fewer intermediaries involved, overall costs are often lower than traditional international bank transfers.

Availability Comparison

Bank Transfers

Bank transfers require:

- Bank accounts

- Banking infrastructure

- Banking hours

Access may vary by country.

Some regions face:

- Limited banking access

- Slower international payment systems

USDT

USDT is available globally wherever supported platforms and wallets exist.

Advantages include:

- 24/7 access

- Borderless transfers

- No dependence on banking hours

This is particularly useful for freelancers, digital nomads, and international businesses operating across different time zones.

Transparency Comparison

Bank Transfers

Tracking international payments can sometimes be difficult.

Users may not always know:

- Where the payment currently is

- Which intermediary bank is involved

- Why delays occur

USDT

Blockchain transactions are publicly verifiable.

Users can:

- Track transaction status

- Verify confirmations

- Monitor transfer progress

This creates a significantly higher level of transparency.

Security Comparison

Bank Transfers

Banking systems are heavily regulated and have long-established security frameworks.

Advantages

- Regulatory oversight

- Consumer protection mechanisms

- Mature financial infrastructure

USDT

Blockchain systems rely on cryptographic security.

Advantages

- Immutable transaction records

- Transparent settlement processes

Users should still follow best practices, including:

- Two-factor authentication (2FA)

- Secure wallets

- Phishing protection

When Bank Transfers Make Sense

Bank transfers may be preferable when:

Large Corporate Transactions

Some organizations require traditional banking infrastructure.

Regulated Financial Workflows

Certain industries depend heavily on banking systems and regulatory compliance.

Traditional Business Relationships

Many companies still prefer bank-based payments and accounting processes.

When USDT Makes Sense

USDT may be preferable when:

Speed Matters

Funds can often arrive within minutes.

Global Accessibility Matters

There is no dependency on banking schedules.

Lower Transfer Costs Matter

Especially for frequent international payments.

24/7 Availability Matters

Transfers can occur anytime, including weekends and holidays.

Real-World Use Cases

Freelancer Receiving International Payments

A freelance developer in Vietnam receives payments from a client in the United States.

Using USDT may allow faster access to funds compared with traditional international banking channels.

E-commerce Business

An online seller receives payments globally and needs to move funds quickly between regions.

Stablecoins can simplify international settlement and improve cash flow management.

International Supplier Payments

Businesses paying overseas suppliers often seek:

- Faster settlement

- Lower costs

- Better transparency

USDT can provide additional flexibility.

Digital Nomad

A digital nomad working across multiple countries benefits from borderless payment infrastructure and around-the-clock access to funds.

How HOYAPAY Supports Both Fiat and Stablecoin Payments

HOYAPAY bridges traditional finance and digital assets through a single platform.

Users can:

Receive USD Payments

Collect international payments through USD Accounts.

Manage Multiple Currencies

Hold and exchange funds efficiently.

Transfer Funds Globally

Move money internationally with greater flexibility.

Access Virtual Cards

Pay for subscriptions and online services.

Use Stablecoins

Manage USDT alongside traditional financial tools.

This flexibility helps freelancers, creators, digital nomads, remote workers, and global businesses operate more efficiently.

Frequently Asked Questions

Is USDT faster than a bank transfer?

In many situations, yes.

USDT transactions can settle within minutes depending on the blockchain network.

Is USDT cheaper than international bank transfers?

Costs vary, but USDT often involves fewer intermediaries and lower overall transfer costs.

Can businesses use USDT for international payments?

Yes.

Many businesses use stablecoins for cross-border transactions and global settlements.

Is USDT available 24/7?

Yes.

Blockchain networks operate continuously.

Which USDT network is best?

TRC20 is often chosen for its lower fees and fast transaction confirmations.

Can freelancers receive payments in USDT?

Yes.

Many freelancers use USDT for international payments because of its speed and flexibility.

Can I convert USDT into fiat currency?

Yes.

Many global payment platforms support conversion between stablecoins and fiat currencies.

Is USDT replacing bank transfers?

Not entirely.

Both systems serve different use cases and often complement each other.

Final Verdict

Bank transfers remain a foundational part of global finance.

They continue to play an important role in corporate payments, regulated industries, and traditional banking relationships.

However, stablecoins such as USDT are reshaping international payments by offering:

- Faster settlement

- Global accessibility

- 24/7 operation

- Reduced reliance on intermediaries

- Improved transparency

For freelancers, digital nomads, remote workers, global businesses, and international entrepreneurs, USDT has become an increasingly attractive option for cross-border payments in 2026.

Ultimately, the best choice depends on your payment needs, preferred financial infrastructure, and operational requirements.